Can Incorrect DPD Reporting Discreetly Affect Your Credit Score?

Raj was confident he had done everything as requested by his lender when he took out and paid off his bike loan, making all EMIs as due. He even received written confirmation from his bank when his loan would end. So, for Raj, the matter was resolved and a chapter of his financial life finished.

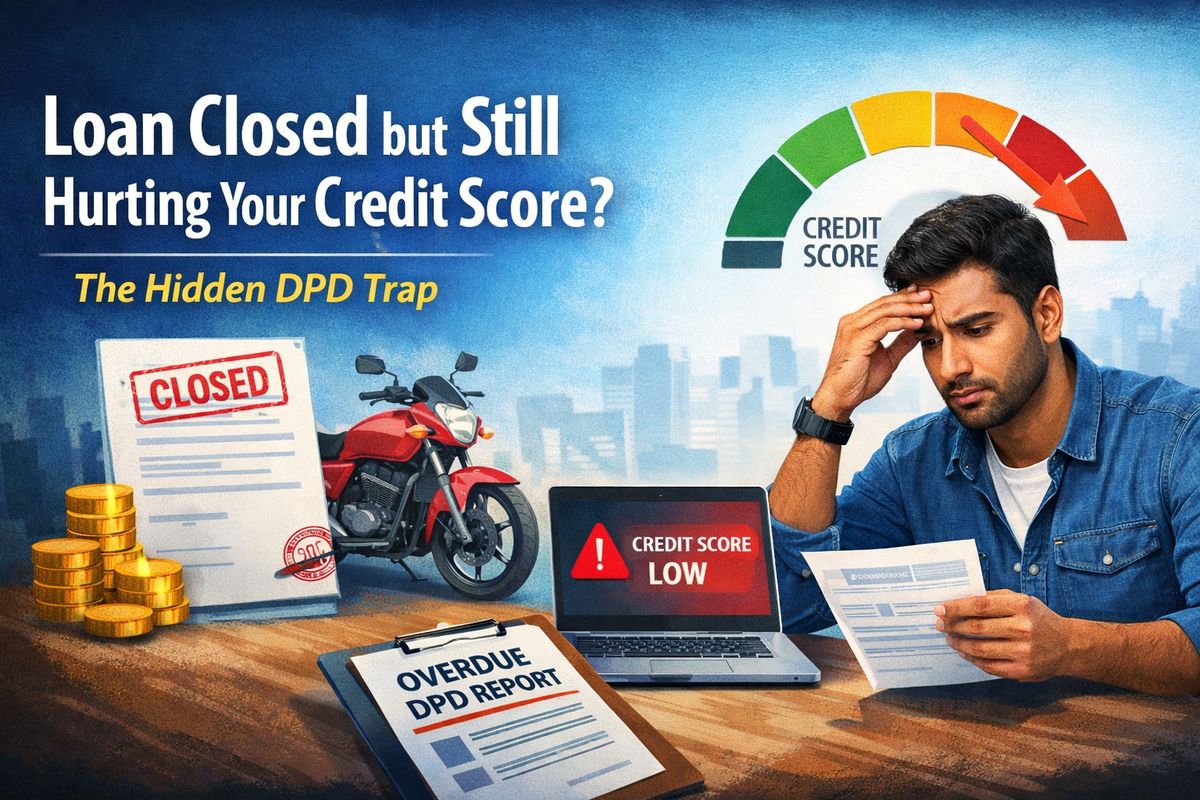

However, approximately one year after paying off the loan, Raj applied for a personal loan to cover an unexpected expense, and the application took longer than he expected to approve. His credit report contained DPD records of his closed loan that continued to be reported as an open account; this is what delayed Raj's loan application.

What happened?

And how many other people like Raj are unaware they will have similar difficulties?

This is Raj's warning and something very few borrowers ever consider.

When a Closed Loan Refuses to Stay Closed

Raj had gotten his bike loan completely paid for. At that point, he had ₹0.00 remaining balance owed, he had not missed any payments, and there were no open disputes regarding that loan account at the time of closure. So, upon receiving the email confirmation of the loan being closed from the lender, Raj believed that all of the formal loan account closure processes needed to close the loan had been completed by the lender.

When Raj applied for a personal loan, however, the lender pulled Raj's credit report and noticed some very concerning information:

The bike loan account – which had been fully paid – had a current status of “active”.

There were multiple months of DPD entries associated with the bike loan.

The bike loan was being reported as overdue – even though it had been fully paid.

From the lender’s standpoint, Raj would look like an individual that has poor repayment tendencies; from Raj’s standpoint — it was a total crisis for him.

Understanding the Importance of DPD

DPD (Days Past Due) measures how many days payments are overdue. Even a small amount of overdue time will be categorized as:

1st – 30th days (Minor Delay)

31st – 60th days (Moderate Risk)

90+ days (Serious Default Risk)

Credit bureaus will report DPD on a month-by-month basis. Continuous reporting of DPDs month-after-month will indicate a pattern of late payments- even though the loan account may no longer be active.

In Raj's case, it wasn't the missed EMIs that were creating the problems; it was the errors in reporting.

How This Error Affected Raj’s Credit Score

Raj’s credit score took a significant hit.

Reasons why reporting incorrect data in your DPD (Days Past Due) to the credit bureaus can have a negative impact on your credit score

The payment history carries the most weight in a credit score

A long history of late payments is a strong indicator of having a high risk

If a loan is closed but reported in error, it could affect your credit score

Lenders do not verify all the information that they use to make lending decisions; they rely on the credit bureaus' data

This resulted in a delay for Raj to be approved for a personal loan, and the lender asked him to "... resolve his credit issues.

Can you imagine being asked to resolve a credit issue that never existed to begin with?

Why Are There So Many Credit Report Errors?

Many borrowers have the misconception that the information on their credit report has been automatically verified for accuracy by the credit bureaus. This is not always the case.

Some of the most common reasons for reporting errors include:

Lenders not updating the status of an account in a timely manner to the bureaus

Technical errors between lending and each of the three bureaus

Manually entered data errors

Transfers of loans between banks and non-bank financial institutions (NBFCs)

Poor post-closure processes

Credit bureaus only show what lenders report, they do not independently verify if a loan is closed.

How Raj Could Have Detected This Earlier

Raj only became aware of his issue when he sought out another loan. By that time, the harm had already been done.

The situation could have been averted if he had:

Checked his credit report on a regular basis

Verified with his lender that his loan was closed after he made the final payment

Looked at the status of his loans to see whether they were "Closed" or "Settled"

Monitored the DPD columns for previous accounts

Doing these things every two to three months can eliminate significant amounts of future issues.

What To Do If You Face the Same Problem

If you have experienced how Raj's loan status affected your ability to obtain future credit, here's what to do:

1) Gather your documentation

Keep a copy of the Loan Closure Certificate, No Dues Certificate, final payment receipts and any communications you may have had with your lender.

2) File a dispute with the Credit Bureau

You can file a dispute regarding an incorrect DPD entry for your closed loan with the following bureaus:

CIBIL

Experian

Equifax

CRIF High Mark

Be specific that your loan is closed and there were no DPD entries and provide any supporting documentation you may have.

3) Follow up with your lender

At the same time you file your dispute with the above credit bureaus, file a complaint with your lender, asking them to complete job responsibilities by correcting the loan status and informing the credit bureaus of their obligation to show your loan as closed.

4) Track the Resolution Timeline

Monitoring for resolution via each dispute requires 30-45 days for completion; if they are not resolved as requested, escalate via the grievance procedure.

How a single credit report inquiry can avoid 3 months of pain

Raj's experience illustrates a very important point:

Your credit health does not end when a loan is paid off. Often times, borrowers are focused on repaying borrowed money but have very little knowledge of the information that gets reported back to the credit bureaus. To that end, the credit report is your financial identity and it requires that you keep up with it by reviewing it regularly.

By checking your credit report, you can:

Find out if there are errors before they become problems

Protect your credit score

Prevent surprise denials of your applications for credit or loans

Keep your eligibility for new loans in an acceptable range.

Raj was able to resolve the issue, however, it did take considerable time and effort and caused him unnecessary stress. Raj's situation teaches borrowers the importance of checking their credit report for accuracy, even after they believe they have satisfied the loan. A borrower can check their credit report for any closed loan whether it was a bike loan, personal loan, credit card or any other EMI to verify that it has been reported as paid off and remains so.

All closed loans should have no further effect on your credit. No closed loan should have any affect on your credit because of the negative reporting of a lender.

Ready to compare real offers?

One application. 10+ RBI-registered lenders. Free for borrowers.