Why Your CIBIL Score Is More Important Than You May Imagine Your financial life depends on your credit score. Your credit score frequently influences the outcome of your loan, credit card, or interest rate applications. The most widely accepted and reliable score utilized by banks and lenders in India is the CIBIL score. You have a significant advantage if you know how your CIBIL score is determined. It increases your chances of getting a loan approved and gives you more financial options. This guide explains everything you need to know in an easy-to-understand manner, including what a CIBIL score is, how it is calculated, what affects it, and how to check and improve it.

A CIBIL Score: What Is It?The three-digit CIBIL score, which ranges from 300 to 900, indicates how well you handle your credit. It is computed by Experian CIBIL, one of the top credit bureaus in India. Lenders view your credit profile more favorably the closer your score is to 900.

Lenders usually see your score as follows:

750 and higher : Excellent, better interest rates and increased chances of approval

700–749 : Good, likely to be approved; below 700: risky, potentially challenging to get approved

Below 550 : High-interest, poor, and limited credit options Your CIBIL score is not arbitrary.

It is determined by your credit behavior, including how you borrow money, pay it back, and manage your money.

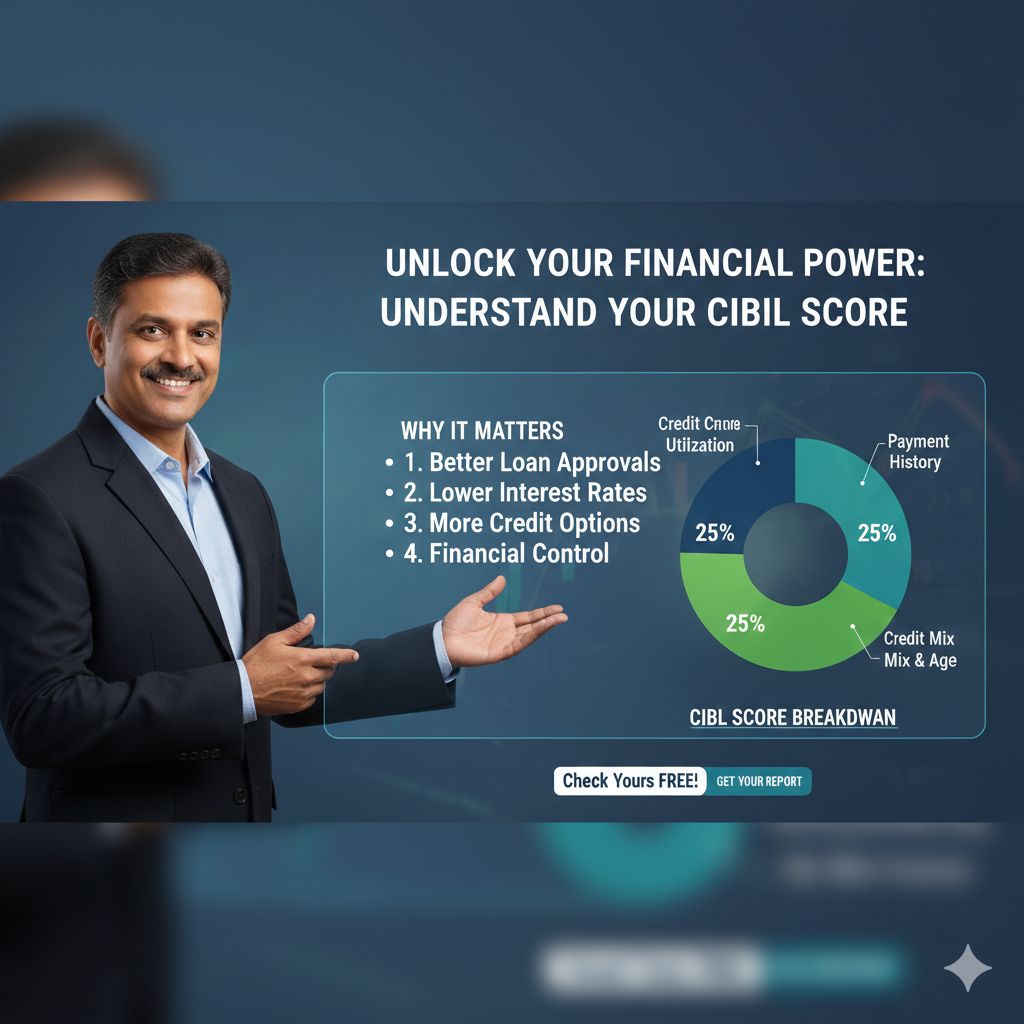

How Do You Determine Your CIBIL Score?Have you ever wondered, "How is my CIBIL score calculated?" It's easier than it looks, so don't worry. CIBIL examines your Credit Information Report (CIR) and evaluates your long-term financial practices. It assesses your overall credit habits rather than focusing on a single error. The distribution of the weight is as follows:

History of Payments (30%) Your credit score increases when you pay your credit card bills and EMIs on time. It can be rapidly reduced by settlements, defaults, or late payments.

Utilization of Credit (25%) This indicates the amount of your available credit that you are utilizing. Better financial control is indicated by lower usage.

Age and Mix Credit (25%) You gain from having a longer credit history and a balanced mix of unsecured credit (cards, personal loans) and secured credit (home, auto loans).

Other Elements (20%) include freshly opened accounts, hard inquiries, and numerous loan applications. As banks and lenders report your activity, your score is updated on a regular basis. Thus, adopting positive habits now can eventually raise your score.

1. History of Payments (30%) This is the most crucial element. Your score can be negatively impacted by even one missed EMI. You can lose up to 100 points for even a 30-day delay. It examines: EMI consistency of payments Payment of credit card bills Loan settlements or defaults Write-offs

2. Ratio of Credit Utilization (25%) This contrasts the amount of credit that is available with the amount that you are using. Experts advise limiting it to less than 30%. Try not to regularly spend more than ₹30,000, for instance, if your card limit is ₹1,00,000. Stress related to money is indicated by high usage.

3. Mix and Credit History (25%) Trust is increased with a longer credit

history. A balanced credit mix demonstrates your ability to manage various loan kinds sensibly.

4. New Credit & Hard Inquiries (20%) Applying for multiple credit cards or loans in a short period of time results in numerous hard inquiries, which can lower your credit score. Lenders may become suspicious if you open too many new accounts.

How Can You Check Your CIBIL Score?By regularly reviewing your credit score, you’ll be better prepared financially for any eventualities. There are a variety of easy methods to keep track.

Click on “Get Your Credit Score.” Put in your personal information and verify via OTP to view either your free credit report or one of their paid plans.

Your bank may also provide access to check your CIBIL score at no cost through internet banking or mobile banking.

Several approved fintech platforms allow users to receive their CIBIL scores free of charge, usually once a month or once per quarter.

Having knowledge of your CIBIL score allows you to have control over your financial future. Your score is not static because it changes as you pay bills on time, maintain a low credit usage ratio, and limit your requests for new loans. This means that you may build up a good credit profile over time. Alternatively, late payments and high levels of debt will cause your CIBIL score to drop rapidly.

If you need capital assistance, consider Samridhya Personal Loans. They offer highly competitive interest rates based upon your credit rating. Additionally, with flexible repayment options, rapid approval times, and minimal paperwork, you can access funds when you need them while continuing to build a positive credit history by making regular payments on time.

FAQ(frequent Answers and Questions)

1. What is a CIBIL Score?

A CIBIL score is a three-digit number that represents how effectively you can manage your credit.

Why is a CIBIL Score Important?

The lenders will use the CIBIL score when evaluating applications and determining approval and limit and interest rates.

What is A Good CIBIL Score?

Most lenders consider scores of 750 and above as excellent.

Who Provides and Maintains the CIBIL Score in India?

Experian CIBIL provides CIBIL scores in India and calculates the scores based on the customer’s credit data.

What Has the Most Impact on a CIBIL Score?

Your Payment History has the largest effect on your CIBIL score.

What Is an Acceptable Amount of Credit Utilization?

The ideal credit utilization percentage should be less than 30% of your maximum credit limit.

Do Late Payments Affect the CIBIL Score?

Yes, a single delay in paying your installment can cause a significant drop in your CIBIL score.

8. Does Multiple Loan Applications Affect the CIBIL Score?

Yes, repeated loan or credit applications have the potential to decrease your CIBIL score significantly.

Can A Low CIBIL Score be Improved?

Yes, consistent and on-time payments and controlling your credit usage will assist in increasing your CIBIL score.

How Can I Get My CIBIL Score?

You can access your CIBIL score online through banks and authorized websites for free.

#personal finance#hard inquiries#credit utilization#emi delays#banking issues#financial awareness#loan rejection#credit report errors#cibil problems#credit score issues ShareReady to compare real offers?

One application. 10+ RBI-registered lenders. Free for borrowers.