Neha’s Story: The Holiday Payment Trap That Hurt Her Credit Score

Neha was always careful about her finances. She worked as a freelance graphic designer, and her monthly income could vary quite a bit. Neha always made sure to pay off her entire balance on her credit card as soon as she was paid, often before the due date.

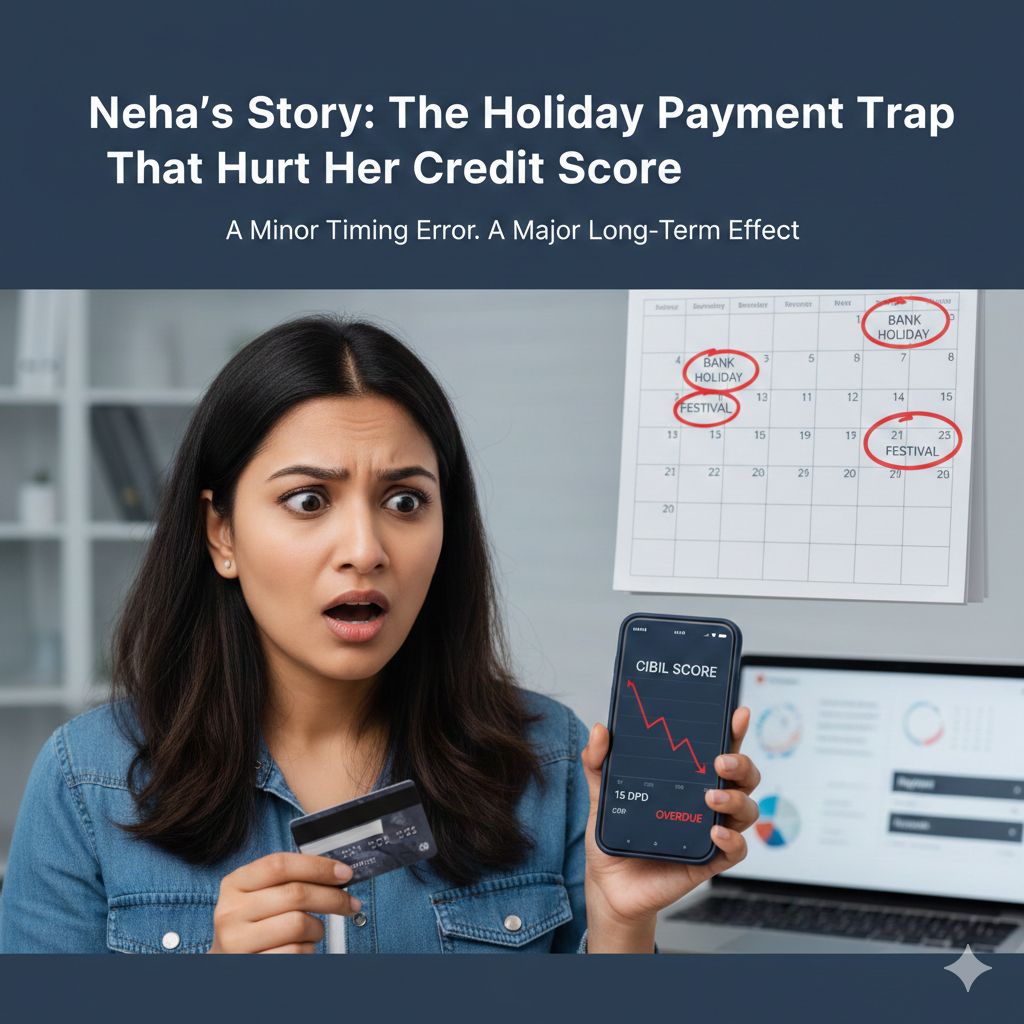

One month, two days prior to when her credit card payments were due, Neha logged into her internet banking and paid her total balance. The money came out of her bank account immediately, so she believed her balance was paid in full.

Unfortunately, one of these two days turned out to be a bank holiday.

What seemed like simply a timing issue turned into a significant credit issue for several months.

What Does “Paid On Time” Mean?

Although the amount was deducted from Neha’s account right away, her credit card company processed the payment after the next business day due to the bank holiday. Therefore, the credit card company acknowledged the payment after it was due.

From the bank’s system point of view:

Payment credited: Late

Account status: Overdue

Days Past Due (DPD): 15

From Neha’s point of view:

Payment initiated before due date

Amount debited successfully

No failure or reversal

No warning or alert

No Warnings, No Alerts, No Second Chances

Neha's situation was made even worse because there was zero communication.

She did NOT receive:

A text message for a late payment

An email for an overdue payment

A telephone call from the bank

A reminder of the payment again

At that point she thought she was doing just fine.

She used her credit card properly, made all subsequent payments on time, and has never been late for another payment. Time passed and she forgot about this incident until she looked at her CIBIL report.

The Shock In Her CIBIL

Neha was preparing to apply for a mortgage and thought she would check her CIBIL report - something she had not previously done and most lenders will only do this before any important milestone in the loan process.

That's when she saw it.

Two things:

15 DPD for payment,

15 DPD was reported

Credit score will be lower than expected.

Neha was shocked! She had NEVER missed a payment. However, her CIBIL shows something different.

Understanding Holiday Payment Trap

Neha’s situation is not an isolated one but typical of a common credit reporting dilemma which is referred to informally as the holiday payment trap. This occurs when:

1) You pay your credit card bill RIGHT BEFORE THE DUE DATE.

2) The payment is made via Online Banking or other Banks.

3) The money transfers after a BANK or HOLIDAY therefore causes an operational delay in the realization of your payment.

4) The Credit Card Issuer does not mark the payment received THE NEXT WORKING DAY (after the holiday).

5) The Credit Bureau views this as a Delinquent Payment.

6) A Direct Payment Entry is reported on your Credit Bureau report and will stay there for many years.

7) When a Direct Payment Entry is made because of being late (usually less than 30 days), the Credit Bureau sees it as a Delay in payment behavior and will therefore REDUCE you credit score.

8) A Credit Bureau will ONLY HAVE a direct late payment if the Issuer's INTERNAL Policy provides for such a delay.

The credit Bureau does NOT look at intent. They look at PAYMENT PATTERNS. For example, with a Direct Payment Entry of 1 for less than 15 days; This event can lead to high interest rates (due to lower credit scores) and higher chances of being treated as a Higher-Risk Borrower by a LENDER (because of credit history).

Risks for Independent Contractors/Self-Employed Individuals When Seeking Financing

Due to their uncertainty of long-term sustainability, independent contractors are scrutinized more stringently than employees by lenders.

Characteristics of independent contractors include:

Volatility in their income

Limited documentation of their fixed income

Higher perceived risk associated with the absence of an employer

When an independent contractor has a credit report that is somewhat late for any reason:

Lenders become more careful

There are more requirements for documentation

The speed of processing loans slows down

If an independent contractor has a delay on their credit report, it can erase several years of disciplined credit history.

The Significant Need/Problem of Technical Delays Related to Credit

Most credit reporting systems use automation; thus the systems do not ask or consider, i.e.

1. Was there a holiday in the banking industry?

2. Were these payments created differently?

3. Was the delay due to something not on the part of the independent contractor?

The information is then recorded in the credit reporting system in the following way:

Date the payment was due

Date the payment was recorded

Difference between both dates

When the payment was recorded after the date the payment was due, the payment will automatically be flagged as late unless corrected manually by the lender, which makes it likely that the independent contractor will not realize that there is an issue until they check their credit history much later.

What Neha Could Have Done (And What You Can Do):

Neha is still unable to change what has happened in the past; however, this event shows that Neha’s lessons may be beneficial for anyone.

1. Pay Your Bills Early, Not Close To The Due Date

When paying your credit card bill, try to pay it three to five working days prior to the due date, especially when using other bank's net banking.

2. Holiday Due Dates

Be cautious of due dates around the holidays. Be aware of:

Bank holidays

Long weekends

Festival holidays

Payments made on or around these dates may take longer to be processed.

3. The Instant Credit Option

If you are paying close to your due date, consider the instant credit options:

Use the card issuer's mobile application

Use UPI linked directly to the credit card

Make a transfer using the same bank

All of these options will typically result in instant crediting of your account.

4. Monitor Your Credit Report

Don’t wait for your loan application to review your CIBIL report. Monitor your report at least every three months to identify and correct any errors before it is too late to correct them.

Concluding Thoughts: Minor Timing Error, Major Long-Term Effect

Neha took every possible step discussed by the moneylender that was expected of a good borrower (i.e. billing early; have money available) as well as trust that the financial system would reciprocate.

However for Neha, the system did not reciprocate.

This example of Neha's case serves as a real life example showing an unfortunate truth about credit reporting practices that even the smallest of technical delays in paying will have significant long term implications for your overall credit scores from your financial history.

When you are able to identify those hidden traps (and how to avoid them), you will be better able to protect your credit score, loan eligibility and future financial goals.

And ultimately, timing in credit reports is not just important; it is everything.

Ready to compare real offers?

One application. 10+ RBI-registered lenders. Free for borrowers.