In India, finding instant cash using a loan against your gold is one of the quickest ways to obtain cash. Whether getting funds for your business, paying for unexpected medical expenses, getting money to pay for fees for education, or just needing short-term cash flow, using gold jewelry as collateral will allow you to get money quickly without having to do a lot of paperwork.

But because many people think that it is quick and easy to get a gold loan, they do not understand the risks that they may be taking.

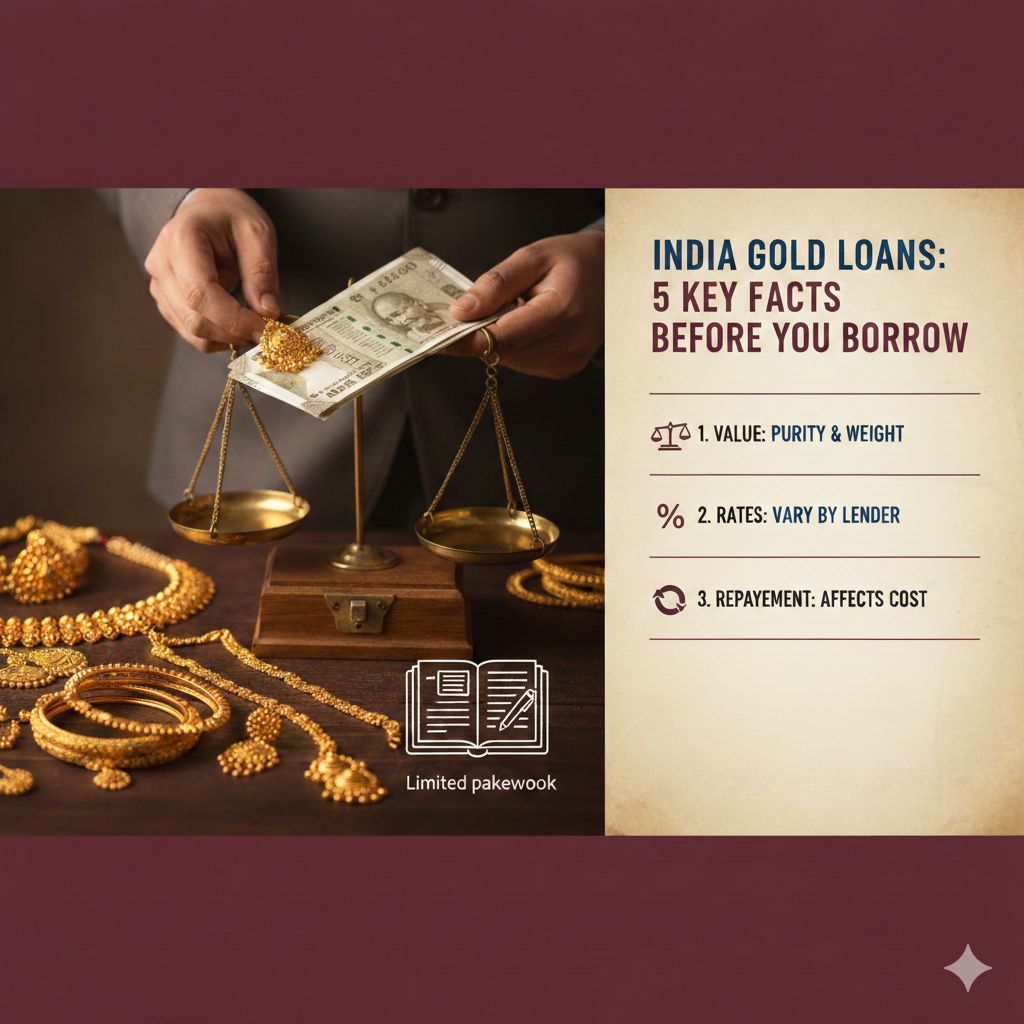

You need to know the following five things before making an application to get the most from your loan:

1. The Amount of the Loan is Based on Both Purity and Weight

The amount you will receive in a loan will not be based only on the market value of your gold, but will mainly be based on:

Purity (karats) of your gold,

Net weight of your gold (not including the weight of any stones, etc.),

The market price of your gold at the time of obtaining the loan, and

The standard loan-to-value ratio that is stated by the lender to the Reserve Bank of India.

Most lenders will provide you with a loan that is 75% or less of your total Gold value, according to Reserve Bank of India guidelines.

⚠️ Important: Any stones or artificial parts are not included in the value of your Gold.

2. The Interest Rate On A Gold Loan Can Vary Greatly From One Lender To Another

Many borrowers think that gold loans always have low-interest rates; however, interest rates will vary from lender to lender as a result of the fact that lenders can freely set interest rates at their discretion.

Lenders will promote their loan with low-interest rates, when in actuality they may have many additional fees associated with obtaining a gold loan, such as:

Processing fees,

Valuation fees,

Late payment penalties,

Auction fees, etc.

Sample Comparison

Lender Type | Interest Rate (Approx.) | Processing Fees | Risk Level |

Banks | 8% – 12% | Low | Safest |

NBFCs | 10% – 18% | Medium | Moderate |

Local lenders | 18% – 36% | High/Hidden | Risky |

Always calculate the total cost of the loan, not just the interest rate.

3. How You Repay Will Affect Your Overall Cost of Borrowing

A gold loan has many options for how to repay a loan. However, if you select an unsuitable repayment method you could increase the burden on yourself based on the choice you selected.

Typical repayment types are:

Bullet repayment: Pay principal + interest all at once, at the end of the term.

EMI repayment: Pay monthly installments of principal + interest.

Interest-only payment: Pay interest only monthly, while deferring payment of the principal to later.

Overdraft facility: Pay interest only on whatever is borrowed.

Helpful Hint:

If you have a fixed reliable income – Select an EMI option.

If you have a temporary emergency – Select a Bullet repayment option.

4. Failure to Repay Could Mean Auctioning of the Collateral

Borrowers often ignore this important detail about the implications of failing to repay a loan.

If you are unable to repay your gold loan, this is what happens:

You will receive written notice from your lender that you have failed to repay.

A "grace period" will be provided for you to pay your loan.

Your gold will be auctioned to recover the loan amount.

You will not lose your gold until the lender gives you multiple opportunities to repay the loan before they will auction the gold to recover the loan.

If the gold sells for a greater value than your loan amount the lender will return to you the difference.

You should only borrow the amount that you expect you will be able to repay.

5. Length of Time to Repay the Loan is More Important than Interest Rate

Many borrowers focus only on interest rate, but tenure plays a bigger role in cost.

Short tenure → Less interest → Lower risk

Long tenure → More interest → Higher risk

Example:

6-month loan costs far less than a 24-month loan even at the same rate.

Gold loans are best used as short-term financing tools, not long-term debt.

Final Notes

If utilized correctly, a gold loan is among the most reliable and expedient ways to fund your immediate needs. These loans require limited documentation, rapid processing, and no credit score requirement; however, they also come with a large amount of responsibility.

Before you submit your application:

Ensure an accurate assessment of your gold's value

Seek to compare lenders and loan terms to find the one that best meets your needs

Carefully consider the terms of your loan repayment

Only borrow what is truly necessary

If used properly, a gold loan can quickly resolve an immediate need for cash without compromising your long-term financial stability.

Frequently Asked Questions (FAQs)

1. Do I need good credit for a gold loan?

No. A gold loan is a secured loan, so as long as the lender can value your gold, your credit rating is not important for accepting your application.

2. What happens if I do not make my first EMI payment on time?

You will incur a penalty from the lender. Continued nonpayment may lead to the lender auctioning of your gold after proper notification in accordance with your loan agreement.

3. Can I repay my gold loan early?

Yes. Most lenders will allow you to pay off your debt prior to the original loan term without incurring a prepayment penalty or fee, and will generally not charge you a fee if you repay your loan in full prior to the scheduled due date.

4. Will my gold be safe while it is held by the lender during the duration of my loan?

Yes. Gold will be safely stored by the lender in state-of-the-art, insured vaults that have restricted access and are monitored by highly trained staff.

5. Can I use my gold coins or bullion to obtain a gold loan?

Generally no; as most lenders will only collateralize against gold jewelry. Certain coins and bullion with proper approvals may be accepted, however, this varies from lender to lender.

Ready to compare real offers?

One application. 10+ RBI-registered lenders. Free for borrowers.